Target next-day settlement. Direct to your UK bank.

Captured Monday by 5pm, the aim is Tuesday morning.

£0

No per-transaction fee. No dispute fee or minimum.

Others charge 20p per transaction. Disputes £15. Cross-border uplift.

100%

UK-built, UK-hosted. UK rails, no US sub-processors.

Servers in London. UK FCA-authorised payments partner.

Everything other processors hide in the background, Fluxa brings into view.

Six things every UK card processor should ship. Tap a card to see the full product UI.

A checkout with your name on it.

Card, Apple Pay, Google Pay across 13 languages. Hosted on our domain or embedded on yours with three lines of code. Your customers see your business, not ours.

YC

Your Company

yourcompany.co.uk

Secure

£149.00

1 × Pro plan, annual subscription

Expires in14:23

PayPay

or pay with card

you@company.com

1234 1234 1234 1234

MM / YY

CVC

Pay £149.00

Need help?

Encrypted and securePowered byfluxa

Three plans. One flat percentage.

No tiers, no add-ons, no surprises. Every feature on every plan. The fee returned in every API response, before the customer pays.

1.8% flat

Founding

1.8%Flat per transaction · all in

1.8% flat for UK businesses. Custom volume rate below 1.8% above £500k per month.

A workforce of agents watches your account at speeds no human team could match, spotting revenue leaks, drafting dispute responses, taking natural-language commands. Then handing every consequential decision to a human at Fluxa.

Meet the team

Tom Harris

Operations & Support

Live · 24/7

Drafts every chargeback rebuttal end-to-end

Traces any payment across every state and retry

Spots a 3% decline jump and names the cause

Reads webhook logs and tells you what broke

Replies in your tone of voice at 3am

Tom is the agent merchants spend the most time with. Deep traceable access to every transaction, settlement, dispute and webhook on your account. Does the work a junior ops person would take a week to do, drafts in minutes.

What they do

Plain-English answers to product questions, citing your own dashboard

Traces a single payment across every state, retry and fee leg

Drafts chargeback rebuttals end-to-end with the evidence already pulled

Reads your webhook logs and tells you why an integration broke

Writes customer replies in your tone of voice, ready to send

How they help you

Files chargeback rebuttals within hours, not days, before the deadline

Spots a 3% decline-rate jump, names the issuer and product behind it

Catches webhook failures the day they ship, not the week customers complain

Briefs you on a customer’s history before you pick up the call

Hands you a one-line summary instead of forty raw transaction rows

Money decisions · human operator approves

James Carter

Onboarding

In testing · Mon-Sat

Pulls KYB straight from Companies House

Runs PEP, AML and sanctions checks instantly

Writes API examples for your exact stack

Reviews your first ten test charges

Cuts onboarding from weeks to days

James gets you live faster than any payments processor we know of. Runs every check the regulator cares about, walks you through the API in your stack, stays with you through the first month after go-live.

What they do

Pulls KYB data from Companies House and pre-fills the application

Runs PEP, sanctions and AUP checks before they become a delay

Generates working API examples for your specific stack

Reviews your first ten test charges, flags anything off

Day-7, day-14, day-30 health checks after you go live

How they help you

Cuts onboarding from weeks to days for clean-shop merchants

Catches AUP-restricted flags upfront, before you waste integration time

Saves you finding the right docs across three regulator sites

Tells you the day before something needs to be fixed, not the day after

Hand-holds your dev through the first webhook signature verification

Approvals · human operator signs off

Sentinel

Platform Health

Live

Watches every transaction every minute

Catches decline climbs before customers notice

Spots latency spikes before alarms trip

Self-heals what doesn't need a human

Pages a human only when it matters

Sentinel is your eyes on the entire platform every minute of every day. Catches anomalies before they reach customers, self-heals what she can, only pings a human when one is genuinely needed.

What they do

Real-time anomaly detection on every transaction flow

Auto-retries failed webhooks with exponential backoff

Routes around degraded gateway endpoints automatically

Compares decline patterns to your 30-day baseline continuously

Tracks latency p50/p95/p99 across every issuer route

How they help you

Catches a 2% decline climb in the first ten minutes, not next week

Stops broken webhook retries from quietly piling up overnight

Routes traffic around a slow issuer before customers feel it

Pings you only when something needs you, not for every blip

Surfaces the one chart that explains the spike, instead of ten

Anything risky · human operator reviews

Auditor

Revenue Integrity

Live

Verifies every fee against your signed contract

Reconciles settlement to the penny every night

Catches pricing drift the day it lands

Audits your refund and chargeback ledger

Reports any payments partner overcharge inside 24 hours

Auditor is your double-entry conscience. Works through every transaction line by line, validates every fee against your contract, reconciles your settlement to the penny every twenty-four hours.

What they do

Per-transaction fee verification against your contracted rate

Daily settlement reconciliation against your ledger to the penny

Validates interchange and scheme fees against the network tables

Flags discrepancies the moment they happen, not at month-end

How they help you

Catches a 4bps rate-card error before it costs you four figures

Saves you the spreadsheet job of reconciling settlement manually

Spots interchange anomalies that your processor won’t flag for you

Hands you a weekly integrity report you can show your finance team

Tells you on day one if a fee was wrong, not at the next quarterly review

Material refunds · human operator confirms

Compliance

Regulatory Cover

Live

Tracks every FCA and AML rule change daily

Reads new regulations the day they ship

Spots AML signals across the dashboard

Files documents before the regulator asks

Keeps your monitoring inspection-ready

Compliance keeps you on the right side of the FCA, always. Tracks every document, watches every AML signal, reads every rule change, translates regulator-speak into specific actions for your business.

What they do

Pings you 30, 14 and 3 days before any document expires

Drafts SAR submissions when AML signals warrant escalation

Reads FCA policy statements and tells you what to change

Continuous PEP and sanctions screening on your customer base

Maintains a regulatory audit trail you can hand to any auditor

How they help you

You never miss a document deadline, ever

You get the action ("rotate director KYC by Friday"), not the legal text

You never have to read a 60-page FCA policy statement again

You can answer a regulator’s questions on the same call, with proof

You sleep at night knowing AML signals are watched on a continuous loop

SAR submission · human operator authorises

What the AI doesn't decide.

Five agents working at speeds no human team could match. They spot patterns, surface problems, and recommend actions. They don't decide on anything that moves money or changes your account.

Money out

Refunds above your authorised threshold, settlement holds, fee corrections, manual disbursements. A human operator approves every penny that leaves Fluxa.

Account changes

Onboarding approvals, acceptable-use changes, account freezes and unfreezes, KYB outcomes. The agent prepares the case. A human signs it off.

Regulatory action

SAR filings, FCA notifications, sanctions hits, anything that leaves Fluxa for a regulator. Our MLRO reviews and authorises before it goes.

Anything ambiguous

If the agent isn't certain, it stops and pings a human. Default behaviour is escalate, not act. We would rather be slow than wrong.

Every consequential action goes through a human operator at Fluxa, with a timestamped log of every AI recommendation, approval, and override. The agents make the operator faster. They never replace the operator.

Three things merchants ask before they sign.

Pricing, the API, the switch. Tap a card for the full answer.

Savings calculator

What your current processor really costs you.

Headline rates hide the real cost. Toggle the fees you’re paying and see the truth on your monthly volume. Numbers sourced from each processor’s published pricing and verified merchant statements.

Your current processor

Headline rate

Percentage

Fixed (£)

Monthly card volume

Average transaction

Stripe UK

£0

0.0% effective

VS

Fluxa

£0

1.8% flat · nothing else

Your monthly saving with Fluxa

£0

per month

That’s £0 a year back in your bank.

Headline cost£0

Per-transaction fees£0

Card-mix surcharges£0

Disputes & monthly fees£0

Sources & method

Headline rates verified directly from each processor’s official UK pricing page (May 2026): stripe.com/gb/pricing, adyen.com/pricing, worldpay.com/en-GB. Card-mix surcharges from Stripe’s public schedule (1.0% EU, 1.75% non-EU, 2.0% FX), Adyen’s Interchange++ documentation, and verified merchant statement audits for Worldpay. Default card mix assumes 15% EU + 8% non-EU + 20% premium based on UK SaaS averages. Numbers are estimates for comparison only; your actual fees depend on your specific card mix, contract, and any negotiated rates.

Competitor pricing correct as of May 2026 and subject to change. All third-party brand names are the property of their respective owners and are referenced solely for factual price comparison under the UK Business Protection from Misleading Marketing Regulations 2008. Fluxa is not affiliated with, endorsed by, or partnered with any of the processors named.

Every feature, on every plan. And how we compare.

We don’t charge for the things other UK processors meter, gate behind tiers, or bolt on as separate fees. 57 rows, 10 unique to Fluxa. Feature by feature, fee by fee.

Fluxaall plans

Other UK processorstypical practice

Pricing certainty8

Headline rate

1.8% flat, all card types

Tiered by card type

Per-transaction fixed fee

£0

Typically 20-25p

Cross-border / EU card uplift

£0

Typically +1-1.5%

Non-EU international card uplift

£0

Typically +1.5-2%

Currency conversion fee

£0

Typically +1-2%

Premium / corporate card uplift

£0

Typically +0.4-1.5%

Monthly platform / gateway fee

£0

Typically £10-40/mo

Setup fee

£0

Often charged

Payments & checkout8

Visa, Mastercard, Apple Pay, Google Pay

Included

Standard

Hosted checkout on pay.fluxapay.co.uk

Included

Standard

Embedded SDK with shadow DOM isolation

Included

Varies

3D Secure 2, SCA-compliant

Included

Standard

AVS and CVV verification

Included

Standard

Custom colours, logo, auto dark-mode

Included

Often limited

Statement descriptor control

Included

Sometimes restricted

Returning-customer one-click checkout

Included

Often a paid tier

Subscriptions & customer ops7

Recurring billing engine, full SaaS

Included

Often metered (~0.5-0.7%)

Trial periods, coupons, proration, plan changes

Included

Add-on tier

Dunning and smart retry logic

Included

Often a separate tier

Automatic card updater

Included

Often paid add-on

Branded card-update emails

Included

Often paid add-on

Customer portal, self-serve cancel

Included

Add-on or DIY

Payment Links with QR codes

Included

Sometimes metered

Developer & API6

Full REST API, live access from day one

Included

Often gated by tier

Test mode and sandbox, full parity

Included

Sometimes limited

Idempotency keys, server-enforced

Included

Inconsistent

HMAC-signed webhooks, unlimited delivery

Included

Often metered

Webhook replay and 90-day delivery log

Included

Often shorter retention

API playground in the dashboard

Included

Rare

Protection & disputes8

Dispute received fee

£0

Typically £15-25 each

Dispute counter / fight fee

£0

Increasingly charged separately

Refund fee

£0 (full processing returned)

Original fee usually not returned

Evidence captured at payment time

Included

Manual collection, post-dispute

Verifi RDR + Ethoca pre-dispute alerts

Included

Often a paid add-on

Merchant Trust Score, real-timeunique to Fluxa

Included

Opaque risk scoring

Fraud detection rules, network-aware

Included

Often paid tier

Reporting, accounting & security8

Six explicit payment states, real-timeunique to Fluxa

Included

Usually 2-3 implicit states

Fee returned in every API responseunique to Fluxa

Included

Rare

Per-payment cost breakdown + transparency report

Included

Usually summary-only

Settlement reconciliation, every batch

Included

Usually monthly statement

Accountant portal: Xero, FreeAgent, QuickBooks

Included

Sometimes a paid add-on

VAT-ready CSV exports

Included

Often extra

FCA-authorised card processing + UK-only London hosting

Included

Often US-routed

MFA/TOTP, dual approval, full audit log

Included

Often partial

Verified Commercial Identity4

Signed Verified Commercial Identity documentunique to Fluxa

Included

Not offered

Public verification page (your trading record)unique to Fluxa

Included

Not offered

VCI API for banks, lenders, platformsunique to Fluxa

Included

Not offered

Bank-grade commercial identity proofunique to Fluxa

Included

CSV export only

AI workforce6

Revenue Doctor: proactive diagnosisunique to Fluxa

Included

Not offered

Dispute Attorney: drafted rebuttalsunique to Fluxa

Included

Sometimes 30% success-fee tools

Co-pilot: natural-language dashboardunique to Fluxa

Included

Not offered

24/7 monitoring across your account

Included

Manual / human-team only

Audit ledger, fully replayable

Included

Partial logging

Consequential decisions handed to a human

Included

Varies

Support & contracts3

No termination clause

Included

Some impose 18-36mo contracts

No price hikes, your rate is your rate

Included

Subject to change

Direct support from the Fluxa team

Included

Tiered support

“Other UK processors” describes typical UK market practice across the sector, not any specific named provider. Individual processors may price differently. Comparison reflects typical UK card processing practice as of May 2026 and is subject to change. Fluxa is not affiliated with, endorsed by, or partnered with any third-party processor.

What your current processor really costs you.

Headline rates hide the real cost. Toggle the fees you’re paying and see the truth on your monthly volume. Numbers sourced from each processor’s published pricing and verified merchant statements.

Every penny, accounted for.

Most processors say a payment is “processing” and leave it at that. Fluxa shows you which of six states it’s in, in real time, with every transition logged.

PAYMENT_RECEIVED

Customer submits card on checkout

CAPTURED

Funds authorised and held at issuer

SETTLING

On its way to your bank account

SETTLED

Cleared to your bank, receipts match

REFUNDED

Funds returned to customer, ledger closed

FAILED

Decline recorded with full reason

Each state writes to a double-entry ledger that runs independently of the state machine. A payment in CAPTURED but not yet SETTLED is visible, not buried under “processing”.

Strict transitions. CAPTURED can’t skip to SETTLED without going through SETTLING. The state machine refuses moves the card schemes wouldn’t allow.

A double-entry ledger runs in parallel. If state machine and ledger ever disagree, Fluxa alerts before any money moves. Audit trail on the dashboard, exportable as JSON, queryable via the API.

Other processors show you a percentage. Fluxa shows you the interchange, the scheme fee, the payments partner cost, and the margin we keep, on every transaction. Reconcile against Visa and Mastercard’s own published interchange and you’ll find we match it, line by line.

UK consumer Visa debit · refreshed against Visa interchange tables monthly

Every charge response itemises interchange, scheme fee, payments partner, and Fluxa margin as separate lines. The same breakdown shows in your dashboard, API response, and CSV export. Cards are priced from the public Visa and Mastercard interchange tables, refreshed monthly. Every penny on the record.

Live status for every payment. From card to bank, you see exactly where each penny is, and when it’s going to land. Not "pending". A specific time. Tomorrow at 06:00.

Money Timeline/pay_4f8e2a91d3c7b6e

09:14:22 · Tue 1 MayLive

Held at issuer

£120.00

−£2.16 · fee£120.00 from Sarah Chen, Visa **** 4242

arriving in21h 30mWed · 06:00

now

Received

just now

now

Captured

,

now

Settling

,

settled

In bank

,

currentlyCustomer's card just authorised. Funds held at the issuing bank, waiting for capture.

fluxa fee£2.161.80% · pending

Live, not historical. ETA on every payment. Every state, every penny, including the bit Fluxa keeps, on its own line in the dashboard and in the API response.

103 pages, 87 components, 2,500+ automated tests. Built around the question UK businesses asks: where is my money, what is holding it up, who needs me right now.

Money you can see

Money timeline.Every delta on your balance. Fees, refunds, settlements, reserves, adjustments. Most processors hide this.

Cashflow forecast.60-day predictive cashflow from subscription renewals, settlements, refunds, disputes. Includes “lose top three” scenarios.

Per-tx fee breakdown.Row-level cost on every payment. Per-tx rate, scheme fees, effective rate. Export and audit.

Month-end close pack.One-click accountant-ready export. Bookkeeper opens it and does not need to ring you back.

Built for revenue, not just collection

Pre-dispute alerts.Verifi and Ethoca feeds. 24-72hr warning before a chargeback fires. Refund first, no scheme penalty.

Network tokens.VTS for Visa, MDES for Mastercard. 3-5% auth-rate lift, survives card expiry. On by default.

Declines, not codes.Every decline tagged merchant-, issuer-, or customer-fixable with the specific action. A verb, not a raw code.

Cross-merchant fraud.A card-testing attack on one Fluxa merchant blocks those BINs across every merchant in the network.

Trust, made verifiable

No-Surprise-Freezes.Seven days written notice before any account-level hold. Reason, named owner, founder line. Published baseline.

Hash-chained audit.Every action SHA-256 chained, tamper-evident. In-browser Verify Chain walks the trail on screen. FCA-exportable.

5-tier Trust Score.Tiers Excellent through Critical. Each tier has concrete consequences for settlement frequency, reserve, support SLA.

Replay with masking.Session replay with PII masking policy inspectable on the audit page. Only during impersonation or via ticket.

Built for UK businesses

MTD VAT submission.We pull VAT data from settlements, compute the return, submit to HMRC via the bridging API.

VRP and Open Banking.Variable Recurring Payments under a single consent. Pay.UK rails, settled next business day, cheaper than cards.

APP fraud cover.UK PSR mandatory reimbursement regime. Five-day window tracked, 50/50 bank-split, evidence pack maintained for audit.

Capital, no PG.Cash advance against future settlements. Fixed fee, no interest, no personal guarantee. Most UK payments partners demand one.

Built like a product, not a portal

Action Centre.The “what needs me right now” inbox. SLA countdowns, undo banner, severity tags, due-today aggregation.

Revenue simulator.Model revenue impact before you ship. Raise prices, add 3DS, shift dunning. See impact before going live.

Predictive churn.Subscriptions about to cancel ranked by risk score. Signals shown, per-customer prevention playbook attached.

Founder Mode.Single screen, eight numbers, one keystroke toggle. For the mornings when noise is the enemy.

The AI workforce, in your dashboard

AI Daily Briefing.Tom writes a short prose summary at 7am. What moved overnight, what mattered, what to act on.

Decisions log.Dated entries tagged Decision, Watch or Question. Tom reads them when you ask follow-ups later.

Inline ask-Tom.Hover any number or row, hit ?. Tom explains it in the same screen. No second window, no ticket.

Tom’s autonomy dial.Per-task slider from propose-only to execute-then-tell-me. Per task type, per merchant, per amount threshold.

Card details, Apple Pay, Google Pay across 13 languages including Arabic and Hebrew. Hosted on our domain or embedded on yours with three lines of code. Your customers see your business name, not ours, no co-branding, no Fluxa logo.

YC

Your Company

yourcompany.co.uk

Secure

£149.00

1 × Pro plan, annual subscription

Expires in14:23

or pay with card

you@company.com

1234 1234 1234 1234

MM / YY

CVC

Need help?

Encrypted and securePowered byfluxa

Paused

Make it yours

01

Brand Extractor.Paste your domain. We pull your logo, palette, and type. First theme in thirty seconds, no design brief needed.

02

AI Designer.Describe the vibe in a sentence. We build a contrast-checked theme to match, complete with a dark variant.

03

Click-to-edit live preview.Click anything on the preview to edit it. Side-by-side desktop and phone, with a QR code for live mobile preview.

04

Thirty-six panel editor.Typography, palette, spacing, motion, locales, fraud rules, capture mode. Every change versioned, rollback-able, and A/B-testable from the dashboard.

05

Custom domain in one click.Host on pay.fluxapay.co.uk by default, or move to pay.yourbrand.com when you’re ready. Free SSL, automatic renewal, no DNS babysitting.

06

13 languages, two right-to-left.Arabic and Hebrew flip the entire layout. Per-locale translation overrides. Customers see their language, not yours, no extra integration.

07

Conditional fields.A VAT number for B2B routes, a delivery phone for shipped goods, a discount code for affiliates. Rules by country, cart total, or referrer, all in the visual editor.

08

CSS escape hatch.When the panels run out, drop your own CSS in. Scoped to the iframe, CSP-vetted, sandboxed. Pixel-level control for designers who need it, no compromise on the security model.

And plenty more.Theme scheduling, WCAG contrast audits, three embed modes, receipt copy, capture-mode rules. All on a dedicated customisation page in the dashboard. Or describe what you want, and the AI designer builds the lot.

What ships in every theme

Smallest PCI scope possible. Card data never touches your servers. Tokenisation runs in the Fluxa-hosted iframe. You stay on SAQ-A, twenty-two questions a year.

Built for every visitor. Audited to WCAG 2.1 AA on every save. Prefers-reduced-motion aware throughout. CSP-locked against cross-site scripting and injection.

13 languages, two right-to-left. Eleven European languages from English to Norwegian. Arabic and Hebrew with full RTL layouts. Per-locale translation overrides available.

Auto dark-mode, contrast-checked. Detects the customer’s system preference at load. Regenerates a dark variant of your theme. Every colour pair passes WCAG contrast.

Network tokens with auto-update. Visa Account Updater and Mastercard ABU on by default. Cards stay valid through every reissue. Card-on-file revenue does not leak away.

3DS 2 done right. SCA exemptions applied automatically where the issuer allows. Frictionless for the customer where possible. Full liability shift on every challenge.

A/B bucketing built in. No third-party tags or pixels involved. No JavaScript bloat for your customer. Compare conversion across two themes from the dashboard.

Visa, Mastercard, Apple Pay, Google Pay. Roughly 98% of UK card transactions covered. No Amex, no third-party wallets, no BNPL. The four schemes your customers use.

Three clicks for you. One branded email per customer, under your domain. Visa and Mastercard subscribers tap once to re-authenticate their card. Subscribers on Amex or other brands add a Visa or Mastercard. Fully automated. Most subscribers complete within a week.

01

Connect

2 min

Migration

Source processor

Stripe

Adyen

Square

Braintree

Paddle

Other

Restricted API key

rk_live_***********************

Read-only. We use it once. We never write to your Stripe account.

In your Stripe dashboard, go to Developers, then API keys, then Create restricted key. Tick read-only permissions for Customers, Subscriptions, Prices, Coupons, Payment Methods and Invoices. Copy the rk_live_… key and paste it here.

02

Approve plan

1 min

Migration plan

760

Re-authenticate same card

Visa and Mastercard subscribers. 68% are one-tap eligible via Apple Pay or Google Pay.

40

Switch to Visa or Mastercard

Subscribers on Amex, Discover or other brands add a supported card during re-auth.

720 of 800 expected to complete within 7 days. Reminders fire day 3 and day 7.

Fluxa shows exactly what will happen for each customer before you commit. Most subscribers re-authenticate the card they already have. The few on unsupported brands add a Visa or Mastercard. Review the breakdown and click Approve to proceed.

03

Launch

5 min

Branded email preview

From: Acme Retail · billing@acmeretail.co.uk

Quick card update needed

Hi Sarah,

We're moving your Acme Retail subscription to a new payment system. Please confirm your card in one tap below.

Same card, same amount, same date.

Confirm your card

Customise the email subject, body and button text with a live preview. Customers on Amex or other brands see a similar email asking them to add a Visa or Mastercard. Click Launch and the campaign sends from your domain with reminders day 3 and day 7.

Honest about why this works. Stripe doesn't expose card numbers via any API. That's a feature, not a limit. So instead of pretending Fluxa can move card data silently, every customer gets one branded email under your domain. Visa and Mastercard subscribers tap once with Apple Pay or Google Pay (or 30 seconds of card entry) to re-authenticate their existing card. Subscribers on Amex, Discover or other brands add a Visa or Mastercard during re-auth, with a clear note that Fluxa accepts those two networks. 90% complete within 7 days on average. Reminders fire day 3 and day 7. Your old processor stays connected the whole time for refunds on legacy charges.

Underneath the migration

Three merchant clicks.Connect Stripe, approve the migration plan, launch the email campaign. About 10 minutes of your time.

One tap or switch to V/M.Visa and Mastercard subscribers tap once to re-authenticate their card. Amex and other-brand subscribers add a Visa or Mastercard.

Email under your domain.DKIM-signed, from your billing address. Customise subject, body, button text, brand colour. Live preview as you edit.

Old processor stays connected.Refunds on legacy charges keep working there until you decide to disconnect. Zero-risk cutover.

Live progress dashboard.Per-customer state in real time. Sent, opened, completed, failed, expired. No black box.

Read-only, never written.Your Stripe key is used once for reads. Never stored, never writes to your account. Revoke after import.

The most-Googled processor problem is account freezes with no warning. Fluxa publishes the exact consequence ladder, monitored against scheme thresholds in real time. You always know where you stand.

Trust monitor/chenco_uk

Healthy

Live scheme monitoringrefreshed daily

Visa VAMP dispute rate0.05%/0.65%

92% headroom

Mastercard ECP excessive chargebacks0.04%/0.65%

94% headroom

Refund rate vs gross volume0.8%/8.0%

90% headroom

Five-tier consequence ladderpublished · immutable

Healthyyou are herebelow 50% of threshold

SettlementT+1

Reserve0%

Support SLA24h

Watch50–75% of threshold

SettlementT+1

Reserve0%

Support SLA12h

Alert75–90% of threshold

SettlementT+2

Reserve5%

Support SLA8h

Restricted90–100% of threshold

SettlementT+5

Reserve10%

Support SLA4h

Suspendedover threshold

Settlementpaused

Reserve100%

Support SLAimmediate

Reviewed daily · published commitment

Five tiers, predictable consequences from Healthy to Suspended, every tier with a defined settlement timing, reserve % and support SLA. Off-board within 5 days, no clawback: if you choose to leave, you keep your settlement schedule. We don’t hold your money to keep you.

One API call to go live. The fee comes back in the response, before the customer pays. HMAC-signed webhooks with rotation, idempotency keys enforced, 2,500+ tests across 37 suites keeping the state machine honest.

Hosted or embedded checkout, Apple Pay and Google Pay, statement-descriptor control.

Ticketing & bookings

High-volume one-offs, no-fee refunds, dispute evidence captured at checkout.

B2B services & consultancies

Per-transaction fee breakdowns, VAT-ready exports, accountant portal for Xero or FreeAgent.

What we won't pretend to do

Amex acceptance

Different rails, different economics. A global enterprise processor will serve you better.

Multi-currency processing

UK domestic GBP is our scope. If you're charging customers in EUR, USD or 30-odd other currencies, a global enterprise processor fits better.

In-person POS & terminals

Hardware, certifications, distribution: a different company. A POS hardware specialist fits better.

Wallets, BNPL, bank debits

UK card rails are our scope. If you need every method, we're not the right fit.

Not sure if you fit? Email paul@fluxapay.co.uk with a sentence about your business. If we can’t help, we’ll send you to the processor that can. No pitch, no funnel.

I’m Paul, and I founded Fluxa. For as long as I can remember I’ve been the sort of person who takes things apart to understand how they work, then puts them back together better. Systems, software, businesses, all of it. That curiosity has never really switched off, and it is the thread that runs through everything I’ve built.

Before Fluxa I started a company of my own and grew it, over several years, into one of the most established names in its field. I did it the unglamorous way: dealing with customers myself, taking the calls, sorting problems in person, and making sure people were genuinely happy before I called a job finished. It taught me that reputation is not something you can market your way to. You earn it one honest interaction at a time, and you keep it by being the person who does what they said they would.

At Fluxa, product and engineering are mine. The API, the dashboards, the hosted checkout, the SDK, and the fraud and anomaly work are all built and maintained in house, on top of thousands of automated tests so the parts you depend on keep behaving. Charlotte runs compliance and operations, and an AI workforce watches the system around the clock and flags anything unusual faster than a person could.

I started Fluxa because too many UK businesses were paying fees they could not explain and waiting in support queues that never cleared. I have been the small business owner on the other end of that, and I did not enjoy it. Everything we build here is meant to fix one or the other.

Charlotte Craig

Partner, operations, Fluxa

I’m Charlotte. Compliance and operations are mine to run.

I’ve spent my career on the inside of the systems most people never see: banking platforms, HR and people systems, and the compliance frameworks that sit underneath them. It taught me how money and information really move through an organisation, where the risk tends to hide, and why the careful, unglamorous work is the work that matters most. I’m the person who reads the rules properly and then makes them workable, rather than treating them as a box to tick.

At Fluxa that means FCA reporting, anti money laundering monitoring, know your business checks, the decisions on which merchants we take on, and the day to day relationships with our payments partner and gateway. It is the discipline that keeps a payments company standing, and I would rather we got it right quietly than make a noise about it.

My job is simple to describe and hard to do well: make sure that when your money moves through Fluxa, it moves through a company that takes the rules as seriously as you take your business.

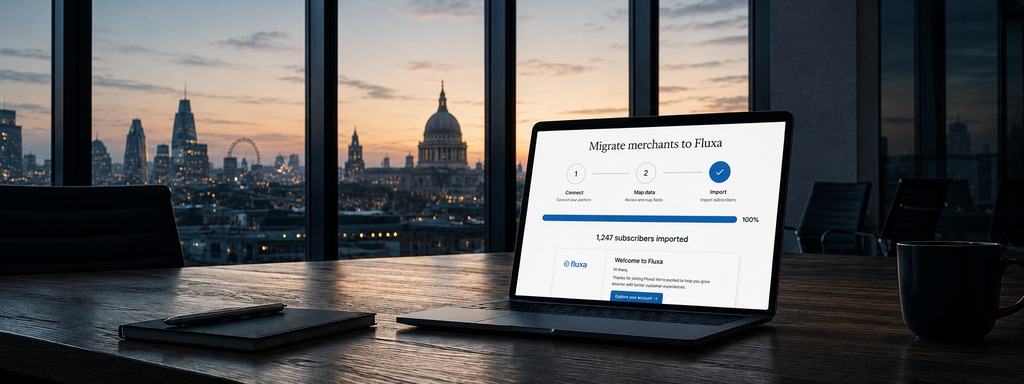

Migration tool ships. Move your subscribers in three clicks.

1 May 2026 · Build

Subscriber migrations used to be a project. Tokens moved by hand, SCA flows tested twice, customers churning during the changeover because the card-update emails landed wrong. The migration tool ends all of that.

Three clicks. Connect your existing processor: Stripe, GoCardless, Adyen, whoever you’re on. Pick the customers. Hit migrate. Branded card-update emails go out under your domain, SCA flows run where the new card needs them, and we chase non-responders on a reminder schedule you control.

Card data never touches your servers. Tokens move network to network and the whole flow is PCI-out-of-scope for the merchant end to end.

A daily progress digest lands in your inbox. A webhook stream tracks the moves as they complete, so your billing platform stays in sync without polling.

Available now to every Fluxa merchant at no additional charge.

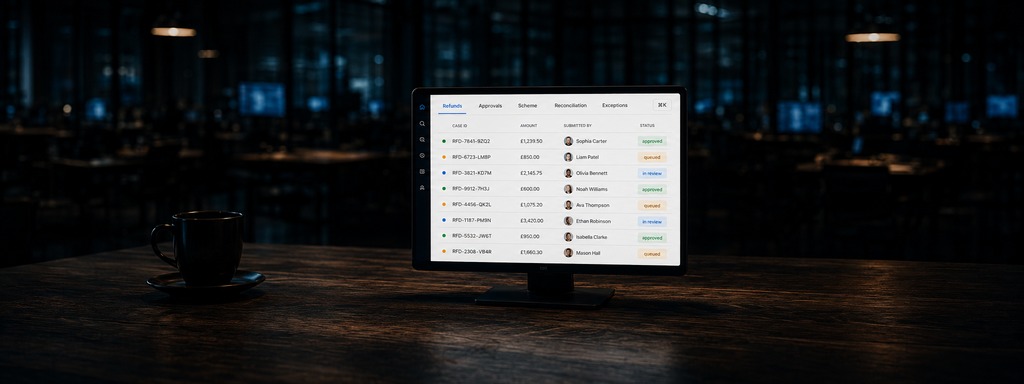

v5.5 puts every internal queue into one workflow. Tickets, approvals, scheme remediation, settlement reconciliation exceptions, compliance flags. One inbox, full keyboard navigation, RBAC on 26 routes, dual-approval token validation on every action that moves money or changes merchant state.

Settlement reconciliation runs in the inbox. When an inbound file doesn’t reconcile to the penny, the discrepancy lands as a workflow item with a side-by-side breakdown, the likely cause auto-tagged by the 19-detector anomaly engine, and a direct route to raise it with the payments partner.

Scheme remediation works the other direction. Visa or Mastercard flag a transaction, it lands in the same inbox with the evidence pack already attached and the response window timed against the scheme deadline.

Numbers behind it: 204 API files, 124 dashboard files, 37 test suites green. Built for the team Fluxa will become, not the team it is now.

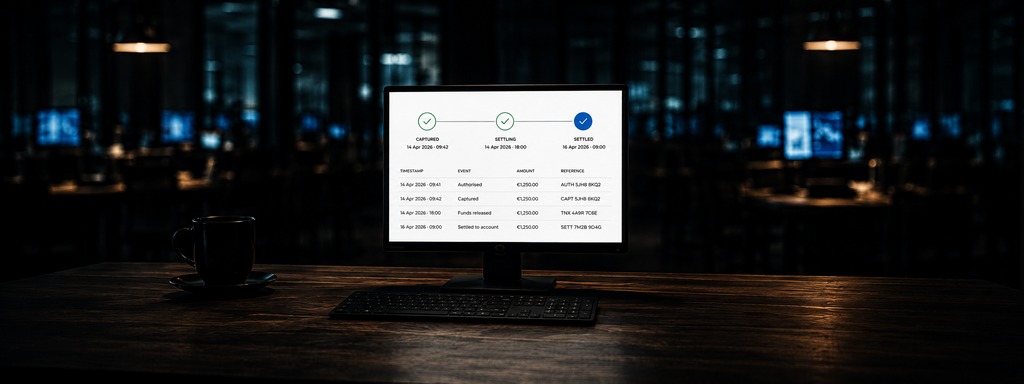

The PFaaS state model is locked. CAPTURED, SETTLING, SETTLED.

14 April 2026 · Architecture

Every payment carries one of three explicit states. CAPTURED: funds authorised, committed, ours to settle. SETTLING: the payments partner is moving the money. SETTLED: cleared into the merchant’s bank account.

State transitions map to specific events: capture authorisation, batch send to payments partner, confirmed receipt of cleared funds. Visible in the API. Visible in the dashboard. Visible in every webhook payload.

No effective-rate fog. No “pending” that means six different things to six different people. No opaque float hiding where the money is on any given day.

Two terminal states close out the model: FAILED and REFUNDED. Five states total. The full lifecycle Fluxa exposes, and the full lifecycle a merchant needs to track.

The architecture is locked. Everything Fluxa ships from here builds on these five primitives.

Founding cohort: 1.8% flat for UK businesses.

7 April 2026 · Cohort

1.8% flat on every transaction, for UK businesses. No plus-twenty-p, no card-type uplifts, no domestic-versus-EU surcharges, no monthly minimums. The rate is written into your merchant agreement.

The maths matters. Stripe’s UK 1.5% plus 20p headline lands between 2.3% and 2.8% effective for most UK B2B SaaS, once you factor in the real card mix and average order value (AOV) the business sees. 1.8% flat beats that effective rate at every realistic AOV, and it’s a single number you can plan unit economics around, on the way up and on the way down.

Founding merchants also get a direct line to the founder. Pricing question, technical edge case, weird thing at three in the morning. The email lands in a founder inbox. Not a queue, not a rep, not a chatbot.

For UK merchants processing £50k to £500k a month. SaaS, digital products, subscription businesses. Anywhere transparent pricing matters more than a rewards points programme.

Featured in FinTech Futures as a notable UK launch.

25 March 2026 · Press

FinTech Futures listed Fluxa among the UK’s notable new fintech launches in March 2026. Cameron Emanuel-Burns wrote the piece, covering the approach to UK SME card processing: flat-rate pricing, transparent payment states, and the choice to launch with the product working rather than the marketing loud.

Trade press read of a launch is the closest thing to a real-world signal you get this early on. This one came in unprompted.

Fluxa builds a signed PDF from your real ledger. The Ed25519 signature covers every page, every value, every total. Tamper one cell and verification fails.

Banks, lenders, and payments partners verify it against our public key, and trust the numbers without ringing you back.

Identity

Matched against Companies House on every page

Volume

Built from your real ledger, transaction by transaction

Regulated UK payments partner. Card processing runs through our FCA-authorised payments partner. Merchant funds sit in safeguarded accounts. Fluxa is the facilitator, not the holder of your money.

Companies House 17028144. Fluxa Ltd is registered in England and Wales. Filings are public, directors are named, the registered office is traceable. Verifiable in real time on the .gov.uk register.

PCI DSS SAQ-A, UK-resident. Card data never touches Fluxa or your servers. Tokenised inside a hosted iframe, processed through a Level-1 certified gateway. All infrastructure sits inside UK borders.

Fluxa is led by Paul Jones, who heads product and engineering, and Charlotte Craig, who heads compliance and operations. They set the company’s direction and its standards, and stay close to the platform day to day, so decisions stay fast and quality stays high.

What’s happening.

Behind the scenes at Fluxa.

First EditionFriday · 1 May 2026 · Vol. I · No. 5

Fluxa NewsIndependent fintech, plainly told.

Build · Migration

Build · Migration

By Paul Jones, Founder

Migration tool ships

Move your subscribers in three clicks. Branded card-update emails go out under your domain. Available now to every Fluxa merchant.

1 May 2026Build

First EditionWednesday · 22 April 2026 · Vol. I · No. 4

Fluxa NewsIndependent fintech, plainly told.

Build · Dashboard

Build · Dashboard

By Paul Jones, Founder

Operator inbox shipped

Admin v5.5 puts every internal queue on one screen. Refunds, approvals, scheme remediation, reconciliation exceptions, all keyboard-navigable.

22 April 2026Build

First EditionTuesday · 14 April 2026 · Vol. I · No. 3

Fluxa NewsIndependent fintech, plainly told.

Architecture · State Model

Architecture · State Model

By Paul Jones, Founder

State model locked in

Every payment now carries one of three explicit states: captured, settling, settled. Visible in the API, visible in the dashboard, no effective-rate fog.

14 April 2026Architecture

First EditionTuesday · 7 April 2026 · Vol. I · No. 2

Fluxa NewsIndependent fintech, plainly told.

Cohort · Founding Rate

Cohort · Founding Rate

By Paul Jones, Founder

1.8% flat for UK businesses

1.8% flat for UK businesses. No plus-twenty-p, no card-type uplifts, no monthly minimums. Direct line to the founder included.

7 April 2026Cohort

First EditionWednesday · 25 March 2026 · Vol. I · No. 1

Fluxa NewsIndependent fintech, plainly told.

Press · FinTech Futures

Press · FinTech Futures

Reported by Cameron Emanuel-Burns, FinTech Futures

Listed as a notable UK launch

FinTech Futures, March 2026. Cameron Emanuel-Burns on flat-rate pricing, transparent payment states, and the choice to launch with the product working.

25 March 2026Press

Migration tool ships. Move your subscribers in three clicks.Bring your existing subscriber list across from any UK processor without a code change. Branded card-update emails, automatic reminders, no card data on your servers, no engineering project.

The dominant UK card processors advertise 1.5% + 20p headline rates, but effective rates for UK SaaS land between 2.3% and 2.8% once corporate cards, international cards, and dispute fees are added. Fluxa is a flat percentage, full stop. The fee comes back in every API response, the buy-rate breakdown sits in the dashboard on every transaction, and a transparency email at month-end shows what you paid versus what a typical processor would have charged on the same volume.

No. One percentage covers every supported card: UK consumer, UK corporate, international Visa and Mastercard, Apple Pay, Google Pay. Interchange and scheme fees do vary by card type, but those sit inside our buy rate, not on top of your fee. For comparison: Stripe adds 1.0% on EEA cards, 1.75% on non-EEA cards, and 2.0% on currency conversion, all on top of headline. Fluxa adds none of that. Your effective rate on a month with 30% international cards is the same as a month with 0%.

For most UK merchants, flat is simpler and more predictable. Interchange-plus is fairer at scale, but it’s a maths problem most teams don’t want: different rates for premium cards, corporate cards, EEA cards, non-EEA cards, plus scheme fees, plus the processor markup, all reconciled monthly against an invoice you can’t verify. We publish the full buy-rate breakdown so you can audit it line-by-line, then charge a single percentage so you can budget. For merchants above £500k a month, where the maths starts to favour interchange-plus, we offer a bespoke interchange-based rate by arrangement.

Yes. Refund a payment, the Fluxa fee is reversed with it. Full refund, full fee back. Partial refund, pro-rata fee back. Most UK processors keep the fee even when the original transaction is reversed, which quietly turns refunds into a cost centre. We don’t. The dashboard shows the reversed fee on the same line as the refund, the API returns it on the refund object, the month-end statement nets it off.

No. Statement descriptor is your trading name, set during onboarding and editable from the dashboard. Your customers see your business on the receipt, on the card statement, on the email confirmation. Fluxa never appears in the customer-facing path. Branded card-update emails for migrated subscribers come from your domain too. We’re infrastructure, not a brand your customers should ever know.

Fluxa processes payments under an FCA-authorised payments partner. All servers in London, double-entry ledger running independently of the state machine. Card data never touches Fluxa or your servers. Under PFaaS, Fluxa doesn’t hold your funds, settlements go from the payments partner direct to your bank account on the schedule published in your trust ladder.

The payments-partner relationship is the regulated one, and your funds never sat with Fluxa. Under PFaaS, settlements move from the FCA-authorised payments partner direct to your bank, regardless of what happens to us. If Fluxa stopped trading tomorrow, in-flight settlements still complete via the payments partner, your historical data is exportable from the dashboard at any time, and you move to another processor on a clean exit. We don’t hold your money, your customer relationships, or your data hostage.

None. The rate is 1.8% flat for UK businesses, written into your merchant agreement. Pass-through costs are shown clearly where they apply. No per-transaction fee, no monthly minimum, no termination clause.

Ready to get started?

Send us an email to set up your account, or arrange a call to walk through onboarding, integration options, and your go-live date. We’ll reply within a working day. No setup fees, no lock-in.